For Mill Owners and Textile Engineers, “Circularity” or Circular Economy is often dismissed as a buzzword or a marketing gimmick. This is a dangerous misconception. The transition from linear to a Circular Economy is a fundamental industrial shift, comparable to the adoption of automation in the 1990s. It is no longer a choice of “being green”; it is rapidly becoming your “License to Operate” in high-value markets like the EU and North America.

The pressure is coming from two sides: Regulators who are legislating waste out of existence, and Brands who are demanding data-backed sustainability to protect their own margins. If your mill cannot process recycled feedstock or provide digital traceability data, you risk being locked out of the supply chain within the next 3-5 years.

Key Takeaways: After reading this article on circular economy you will know

- Circularity ≠ Recycling: Recycling is just one process; Circularity is the entire system of keeping materials in use.

- The Stick (Regulation): By late 2026/2027, EU regulations (EPR) will financially penalize non-circular textile imports.

- The Digital Mandate: Your ERP must evolve. Without data digitization (Digital Product Passports), your sustainable product is “invisible” to buyers.

- The Standard: ISO 9001 is no longer just for quality; it is your safety net for managing variable recycled feedstocks.

- The Opportunity: The circular transition represents a $560 Billion global opportunity in recovering value from waste.

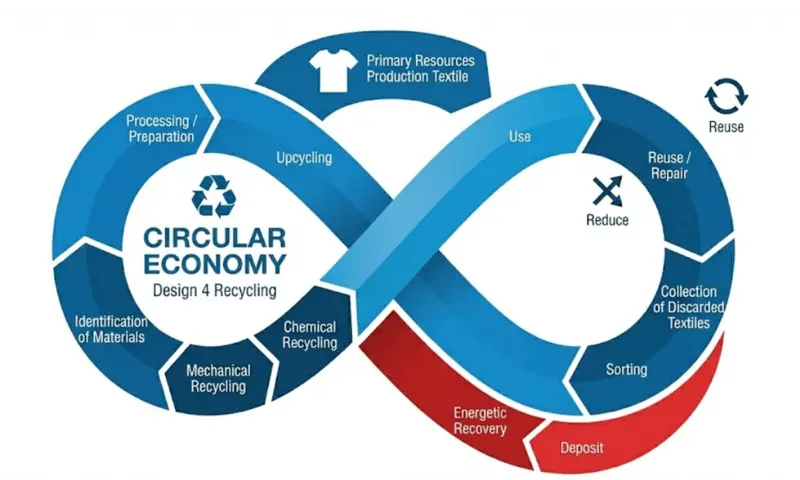

The Definition Reset : What Actually is Circular Economy?

To capture this $560 billion opportunity, we must first dismantle a common industry confusion: the conflation of “Recycling” with “Circularity.” While often used interchangeably, they represent two fundamentally different approaches to industrial production.

Recycling is a Process; Circularity is a System. For decades, the textile industry has relied on mechanical recycling as a crutch. This is typically an “end-of-pipe” solution: taking waste (like cutting scraps or old jeans), shredding it, and spinning it into lower-quality yarns (often called “downcycling”). While better than landfill, this process degrades fiber length and tenacity, eventually resulting in waste that cannot be used again.

The Circular Economy changes the goal post. It focuses on the “Upstream” phase—design and material selection. In a circular system, a product is engineered from the start to be disassembled and regenerated without losing value. It is not just about managing waste; it is about designing waste out of the system entirely.

To standardize this global language, the International Organization for Standardization (ISO) has introduced the ISO 59000 family. This standard moves circularity from a vague marketing term to a rigorous technical framework. According to this framework, a mill operating in a circular economy adheres to three core principles:

- Design Out Waste: Manufacturing processes are optimized so that “waste” (e.g., comber noil) becomes a valuable input for another line (e.g., open-end spinning) or another industry (e.g., non-wovens).

- Keep Products and Materials in Use: Increasing the durability and physical life of the fiber. This means prioritizing fiber blends that can be chemically separated later, rather than complex blends that are destined for the incinerator.

- Regenerate Natural Systems: Ensuring that renewable feedstocks (like cotton or viscose) are sourced from regenerative agriculture that improves soil health, rather than depleting it.

Bottom Line for the Mill: Recycling is asking, “What do I do with this trash?” Circular Economy is asking, “How do I ensure this material never becomes trash in the first place?”

The Regulatory Landscape who is deciding this?

While ISO 59000 provides the definitions, the motivation to adopt them is no longer voluntary; it is being codified into hard law. The era of self-regulation is over. Governments are stepping in to correct market failures, and for the global textile industry, the rules of the game are being rewritten primarily in Brussels.

The Power Player: EU Strategy for Sustainable Textiles As of early 2026, the European Union remains the global legislative engine. The EU Strategy for Sustainable Textiles is not just a policy paper; it is a suite of binding directives that impact any mill exporting to Europe. The core logic is simple: if you want to sell to the EU’s 450 million consumers, your product must be durable, recyclable, and free of hazardous substances.

Two specific mechanisms act as the primary “enforcers” of this strategy:

- EPR (Extended Producer Responsibility): This is the financial “Stick.” Under EPR schemes (mandated by the revised Waste Framework Directive), brands are financially responsible for the end-of-life of their products.

- The Impact: Brands will be charged a fee for every kg of textile they put on the market. This fee is eco-modulated—meaning it is lower for easy-to-recycle products (e.g., 100% cotton) and significantly higher for complex, non-circular items (e.g., poly-cotton blends with elastane).

- Business Reality: Brands will aggressively push these costs down the supply chain, demanding single-fiber compositions to lower their tax burden.

- DPP (Digital Product Passport): This is the “Data Mandate.” By 2027, most textiles entering the EU will likely require a digital record (accessible via QR code) that details fiber composition, chemical usage, and recycled content.

- The Constraint: If your mill cannot prove the percentage of Recycled Polyester (rPET) via traceable data, the product cannot legally enter the market.

Regional Specifics: A Fragmented Map

- The EU (The Leader): Regulations are hard, binding, and imminent.

- The USA (The Follower): Federal action is slow, but states are moving. California (SB 253) and New York are proposing their own versions of fashion accountability acts.

- Asia (The Adapter): In manufacturing hubs like India, Vietnam, and Bangladesh, circularity is Compliance-Driven. There is little domestic demand for circular products, but the survival of the export sector depends entirely on aligning with Western regulatory standards.

The Operational Impact :The Mill Floor Transition

To meet these regulatory demands without facing bankruptcy, the mill floor must evolve from a rigid linear production line to a flexible, “Feedstock-Agnostic” system. This is where the theoretical concept of circularity collides with the hard physics of textile manufacturing.

1. The Shift to Feedstock Agnosticism In the linear era, mills optimized for consistency using high-grade virgin fibers (e.g., contamination-free US Cotton or uniform Virgin Polyester). The circular mill, however, must process input materials with high variability.

- Post-Consumer Waste (PCW): The new challenge. Sourced from used garments, this feedstock often suffers from shortened fiber lengths, varying dye affinities, and foreign matter contamination.

- The Operator’s Headache: A mill spinning 30s Ne using 20% r-Cotton (PCW) will experience significantly higher breakage rates than with virgin fiber unless the process parameters are re-engineered.

2. The ISO 9001 Criticality This variability is why ISO 9001 (Quality Management Systems) is no longer just a “certificate for the wall”—it is your operational safety net.

- Why it matters: In a circular model, raw material parameters fluctuate batch-to-batch. A standard ISO 9001 QMS framework forces you to document and standardize the process of handling these fluctuations.

- The Application: You must implement rigorous Incoming Quality Control (IQC) for waste bales, establishing tolerance limits for short fiber content (SFC) and trash. Without a robust QMS, introducing recycled fiber is not “circularity”; it is simply “contamination” that ruins your final yarn quality.

3. Machinery Adjustments & Physics Processing recycled fibers requires specific mechanical compromises:

- Ring Spinning: Traditionally struggles with the high short-fiber content of mechanically recycled cotton. To maintain yarn strength (CLSP), mills often have to reduce spindle speeds by 10-15% and increase twist multipliers.

- Rotor (Open-End) Spinning: Much more forgiving of short fibers and trash. We are seeing a strategic shift where mills reserve Ring Frames for virgin/blended fibers and dedicate Rotor lines for >50% recycled content products.

The Digital Backbone : ERP & Data Digitization

However, recalibrating your machinery is only half the battle. In the context of the new regulatory landscape of circular economy, if you cannot prove to a brand that your yarn contains exactly 30% recycled cotton using validated data, that physical effort is commercially worthless. This is where the battle shifts from the mill floor to the server room.

The New “Business Need”: Why Excel is Dead For decades, textile mills have run on legacy ERP systems designed for linear flows: you buy cotton, you spin yarn, you sell yarn. These systems treat waste (noil, drop, hard waste) as a “loss” to be written off.

- The Circular Shift: In a circular economy, waste is an Asset. Your ERP must be re-configured to inventory “waste” with the same rigor as virgin fiber. It needs to track a bale of cutting scraps not just as “trash,” but as “Raw Material Type B, Batch #402, 98% Cotton/2% Elastane.”

Traceability & The Digital Product Passport (DPP) The ultimate output of this digitized data is the Digital Product Passport (DPP).

- The Data Requirement: The DPP will not just ask “Is this recycled?”; it will ask “Where did the waste come from?” and “What chemicals were used to recycle it?”

- The ISO Link: Here, your ISO 9001 documentation becomes digital. The Quality Management System provides the procedures for verifying the waste, while the ERP provides the data trail that proves you followed them.

The Cost of Silence We are entering an era of “No Data, No Sale.” Brands facing EPR taxes need your data to lower their own financial liability.

- The Risk: If your mill produces excellent recycled yarn but lacks the digital traceability to prove its origin, you are invisible to top-tier buyers.

- The Investment: This requires upgrading from basic accounting software to specialized textile-specific ERPs or integrating third-party traceability platforms (like tracers or blockchain tokens) that can “tag” the fiber physically and digitally.

The Economics : The Money

Investing in digital infrastructure and re-tooling machinery requires capital, but viewing this purely as an “expense” is a strategic error. To understand the true business impact, Mill Owners must calculate the “Cost of Inaction.” The economics of the textile trade in circular economy are shifting from a “Low Cost” model to a “Total Value” model.

The “Shadow Price” of EPR The most immediate financial impact comes from the Extended Producer Responsibility (EPR) fees. Analysts estimate that under upcoming EU schemes, non-circular garments could attract penalties ranging from €0.15 to €0.50 per item.

- The Business Case: If a Brand is facing a €0.50 tax on a pair of jeans because they use virgin cotton, they will logically be willing to pay a supplier a premium of €0.10 – €0.20 for a certified recycled fabric that exempts them from that tax.

- The ROI: The return on investment for circularity is not just in the yarn price; it is in the tax avoidance value you provide to your customer. You are not just selling yarn; you are selling regulatory insurance.

Market Retention vs. Green Premium A critical “Gritty Reality” to accept is that the “Green Premium” (charging extra for sustainability) is disappearing. It is being replaced by “Market Retention.”

- Scenario: In 2026, two mills offer fabric at $4.00/meter. Mill A offers standard virgin fabric. Mill B offers traceable, 20% recycled fabric with ISO 9001 quality data.

- Outcome: The buyer chooses Mill B not because it is cheaper, but because it solves their compliance headache. Mill A doesn’t just lose the margin; they lose the contract entirely.

Take away

We are witnessing the most profound shift in the textile industry since the Industrial Revolution. The transition to a Circular Economy is not a temporary trend driven by activists; it is a structural reorganization driven by economics and law.

For the Mill Owner, the path forward is clear but challenging. It requires moving away from the comfortable linear model of “Buy Cheap Cotton -> Spin Fast -> Sell Cheap.” It demands a new mindset where waste is an asset, data is a product, and compliance is a competitive advantage.

By adopting the principles of ISO 59000, investing in flexible “feedstock-agnostic” machinery, and digitizing your supply chain, you are doing more than just meeting a regulation. You are transforming your business from a replaceable Vendor into an indispensable Solution Partner.

The mills that ignore this shift will find themselves fighting a losing battle over fractions of a cent in a shrinking commodity market. The mills that embrace it will secure their legacy, their profitability, and their “License to Operate” for the next generation.